What is a Credit Score?

A credit score is a numerical snapshot of how lenders assess your financial reliability.

Scores typically range from 300 to 850, and higher scores signal lower risk to lenders.

Your score directly impacts whether you’re approved for loans, credit cards, or financing—and what interest rate you’re offered.

Lower scores often lead to higher interest costs over time.

Improving your credit profile can reduce borrowing costs and expand your financial options across mortgages, auto loans, and revolving credit.

Scores typically range from 300 to 850, and higher scores signal lower risk to lenders.

Your score directly impacts whether you’re approved for loans, credit cards, or financing—and what interest rate you’re offered.

Lower scores often lead to higher interest costs over time.

Improving your credit profile can reduce borrowing costs and expand your financial options across mortgages, auto loans, and revolving credit.

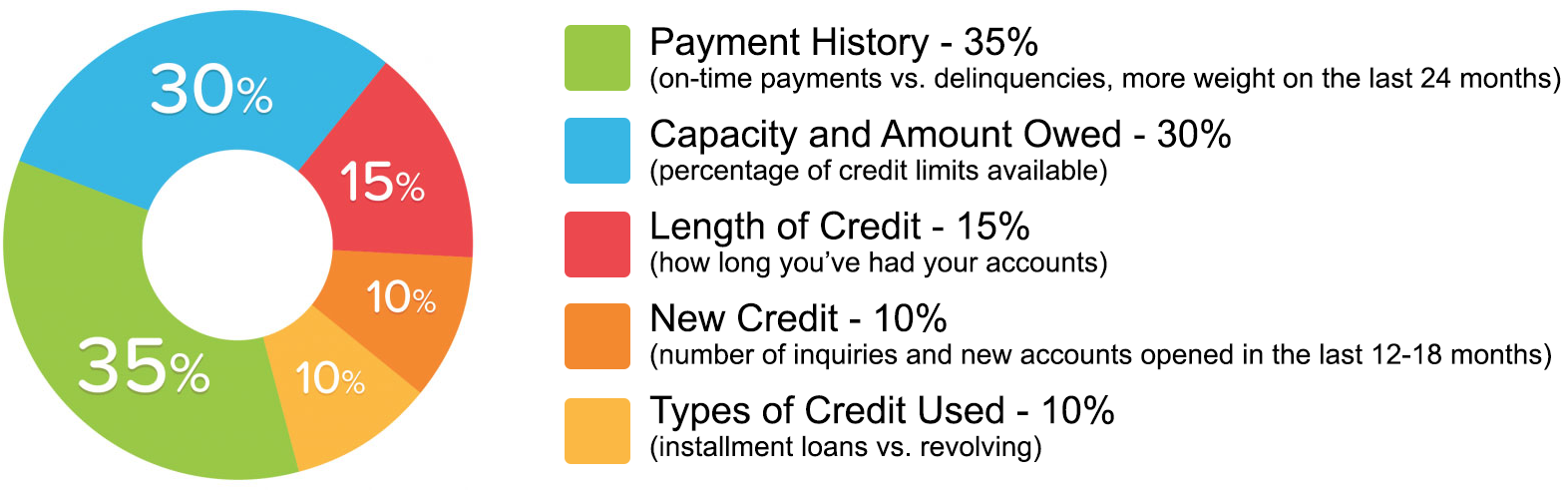

What affects your Credit Score?

How We Address Negative Reporting

- Our process focuses on reviewing credit reports for accuracy, completeness, and compliance with applicable credit-reporting standards. When appropriate, we prepare and submit documentation to request verification or correction of disputed items with the consumer reporting agencies and data furnishers.

What We Support: - Review of reported accounts for potential inaccuracies or inconsistencies

- Preparation of professional correspondence related to disputed items

- Guidance on credit utilization and account management best practices

- Support with reviewing inquiries and understanding how they impact your profile

- Ongoing tracking of responses from consumer reporting agencies

- Important Notes:

- Credit reports may vary between Equifax, Experian, and TransUnion due to differences in how information is furnished and reported.

- Results vary by individual credit profile, reporting history, and creditor responses.

- We do not promise specific outcomes or timelines for score changes or item outcomes.

What You Can Do to Improve Your Credit Profile

Improving your credit profile is a combination of consistent habits and strategic account management. While we handle the reporting and documentation process, your actions play a key role in long-term results.

Best Practices to Follow:

• Pay all accounts on time, every time

• Keep credit card balances below 30% of available limits

• Avoid unnecessary new credit applications

• Monitor your credit reports regularly for inaccuracies

• Use revolving credit responsibly and pay balances in full when possible

For clients who prefer simplicity, using one or two cards for small recurring bills and paying them in full each month can help establish strong payment behavior without increasing debt.

Best Practices to Follow:

• Pay all accounts on time, every time

• Keep credit card balances below 30% of available limits

• Avoid unnecessary new credit applications

• Monitor your credit reports regularly for inaccuracies

• Use revolving credit responsibly and pay balances in full when possible

For clients who prefer simplicity, using one or two cards for small recurring bills and paying them in full each month can help establish strong payment behavior without increasing debt.

How Long Do Credit Items Typically Remain on Your Report?

- Delinquencies (30- 180 days): A delinquency may remain on file for seven years; from the date of the initial missed payment. The length of time items appear on a credit report is governed by federal credit-reporting rules and may vary based on the type of account and the date of first delinquency. Timeframes below are general guidelines: Common Reporting Timeframes:

- Late Payments (Delinquencies):

Reported for up to 7 years from the date of first delinquency. - Collections:

Reported for up to 7 years from the original delinquency date that led to the collection. - Charge-Offs:

Reported for up to 7 years from the original delinquency date, even if the account is later paid. - Closed Accounts:

• Negative closed accounts: up to 7 years

• Positive closed accounts: up to 10 years - Bankruptcy:

• Chapter 7: up to 10 years

• Chapter 13: up to 7 years - Hard Inquiries:

Reported for up to 2 years (typically impact scores for the first 12 months) - Public Records:

Reporting timeframes vary based on the record type and applicable reporting rules - Reporting timeframes may vary by bureau and creditor reporting practices. Removal eligibility depends on accuracy, compliance, and documentation standards.

Information That Should Not Appear on a Credit Report

- Federal credit-reporting law limits what information may be included on your credit report. The following information generally should not appear:

- Medical details

Credit reports may not include specific medical diagnoses or treatment details. - Outdated negative information

Most negative items older than 7 years (and bankruptcies older than applicable reporting limits) should no longer be reported. - Personal demographic information used for employment screening

Information such as race, marital status, age, or religion cannot be reported for credit-evaluation purposes. - Accounts that do not belong to you

Information reported to your file must be accurately matched to your identity. - Information reported without permissible purpose

Creditors and agencies must have a lawful reason to access or furnish your credit information. - If inaccurate, incomplete, or unverifiable information appears on your credit report, you have the right to dispute it under federal credit-reporting law.

Your Rights Under Federal Credit Reporting Law

You have the right to review your credit reports, dispute inaccurate or incomplete information, and receive timely responses from consumer reporting agencies and data furnishers. Federal law requires credit bureaus to investigate disputes and correct or delete information that cannot be verified.

CreditBull Solutions LLC provides structured credit-reporting enforcement services focused on identifying potential reporting inaccuracies, preparing professional correspondence, and managing the dispute workflow on your behalf. Results vary by file and creditor response, but our process is designed to ensure your rights are exercised consistently and properly.

CreditBull Solutions LLC provides structured credit-reporting enforcement services focused on identifying potential reporting inaccuracies, preparing professional correspondence, and managing the dispute workflow on your behalf. Results vary by file and creditor response, but our process is designed to ensure your rights are exercised consistently and properly.